From $130 to $1,800: What the New Student Loan Payment Rules Mean for You

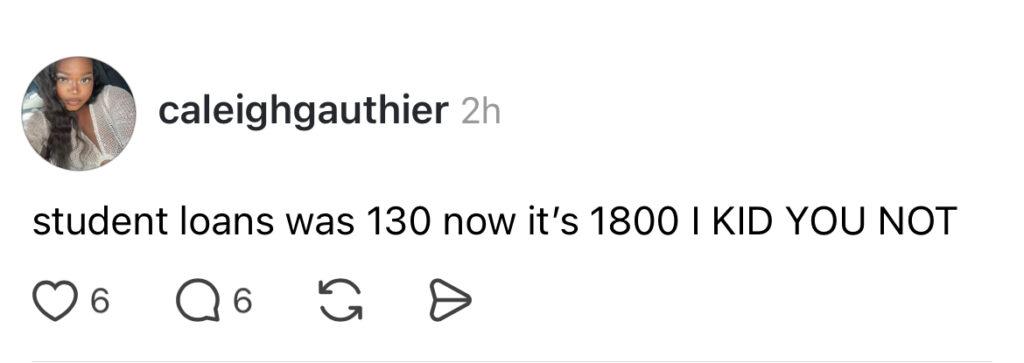

Scroll through social media this week and you’ll find a familiar kind of viral post: a screenshot of a student loan bill, a shocked caption, and a number that doesn’t seem real. One borrower says her monthly payment jumped from $130 to nearly $1,800. Others are sharing similar stories of payments doubling or tripling after years of paying little or nothing.

If those posts gave you a jolt of panic, take a breath. As of today, July 1, 2026, the federal student loan system is going through its biggest overhaul in decades. But most of the scariest headlines apply to a specific group of people, and there’s a good chance you have more protection than those posts suggest.

Why payments are suddenly exploding

The biggest reason behind the viral posts is the end of a repayment plan called SAVE.

SAVE gave millions of borrowers very low monthly payments. Since 2024, nearly 7 million people in the program have been in a payment pause, many paying $0 while it was tied up in court. That pause is now ending.

If you’re one of those people:

- Your loan servicer will start sending notices around today telling you to pick a new plan.

- You’ll have 90 days to choose one.

- If you don’t choose, you’ll be placed into a standard plan automatically, often the most expensive option.

The borrower whose payment went from $130 to $1,800 was likely in SAVE, paying a reduced amount, and is now being moved to a plan that spreads her full balance over a fixed number of years. The jump feels brutal because the old number was artificially low, not because her debt grew.

What to do: Don’t ignore the notice. Log into your servicer’s website, and actively pick a plan instead of letting the clock run out.

The new repayment plans

If you take out a new loan after today, you’ll have two options:

Standard Plan: Fixed monthly payments over 10 to 25 years. Predictable, but not based on your income.

Repayment Assistance Plan (RAP): The new income-driven option. Your payment is set between 1% and 10% of your income, with a floor of just $10 a month for the lowest earners. The catch: RAP doesn’t forgive your remaining balance until you’ve made 30 years of payments, versus 20 or 25 years under the older plans. It can lower your monthly bill but keep you in repayment longer.

New limits on how much you can borrow

Starting today, there are new ceilings on federal loans:

- Graduate students: up to $20,500 per year, capped at $100,000 total.

- Professional students (law, medicine, and similar): up to $50,000 per year, capped at $200,000 total.

- Parents (Parent PLUS): up to $20,000 per year per child, capped at $65,000 total per child.

The Grad PLUS loan, which used to let students borrow up to their full cost of attendance, is also eliminated for new borrowers. If federal loans no longer cover your costs, you may need scholarships, savings, or private loans to fill the gap.

The most important part

If you already have student loans and don’t take out any new ones, you are largely protected for now.

That’s the piece the viral posts leave out. Current borrowers who don’t borrow again keep their existing repayment options. And if you’re mid-degree, you generally keep the old borrowing limits for three more years or until you finish, whichever comes first.

One exception: taking out even one new loan can pull all your loans, including older ones, under the new rules. So if you’re close to done, think carefully before borrowing again.

A bit of good news: Pell Grants

Starting today, Pell Grants, which never have to be paid back, are expanding to cover short-term job training programs that run roughly 8 to 15 weeks, like training to become a certified nursing assistant or welder. For the first time, you can get federal help paying for these without taking on debt. The first step is the same as always: fill out the FAFSA at StudentAid.gov.

What to do this week

- If you were in SAVE: Pick a new plan within 90 days. Don’t let the default choose for you.

- If you have loans and aren’t borrowing more: You’re mostly insulated. Just avoid new loans without understanding the tradeoffs.

- If you’re about to borrow for school: Know the new limits, and that Grad PLUS is gone.

- Everyone: Use the free Loan Simulator at StudentAid.gov to compare plans.

The system is changing fast, but the viral horror stories are usually one specific slice of a much bigger picture. Knowing where you fit is the difference between panic and a plan.

This article is general information, not personalized financial advice. For your specific loans, contact your servicer or visit StudentAid.gov.

You’re Blowing $10,000 a Year and Ain’t Even Know It

Twenty-seven dollars. That’s it. That’s the number that’s quietly running your pockets...

The AI Boom Made History in 2025. Black Founders Were Locked Out of the Room.

If 2024 was the year venture capital quietly walked back its promises...

What Spirit’s Shutdown Means for Your Next Flight

You never flew Spirit. You swore you never would. Doesn’t matter, your...

Flying Soon? TSA Lines Could Be Longer Than Your Flight

Travelers heading to the airport this week are being urged to plan...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment